The numbers are easy to read as an obituary for physical retail.

Discretionary spending growth in Australia is forecast to slow from 2.5 percent to just 0.7 percent into 2026 (Deloitte Access Economics). Clothing, footwear and department stores have posted some of the sharpest monthly falls in the country (ABS). Department-store floorspace is in structural decline, and the trade press is openly forecasting fewer stores (Ragtrader). Meanwhile online keeps taking share: e-commerce penetration is at a record high near 14 percent and forecast to reach 17 by the end of the decade (ABS, CBRE, IBISWorld).

The easy conclusion is that physical retail is finished and everything moves online. I think that is the wrong lesson, and the brands actually winning prove it.

The two jobs

Start by being honest about what each channel is for.

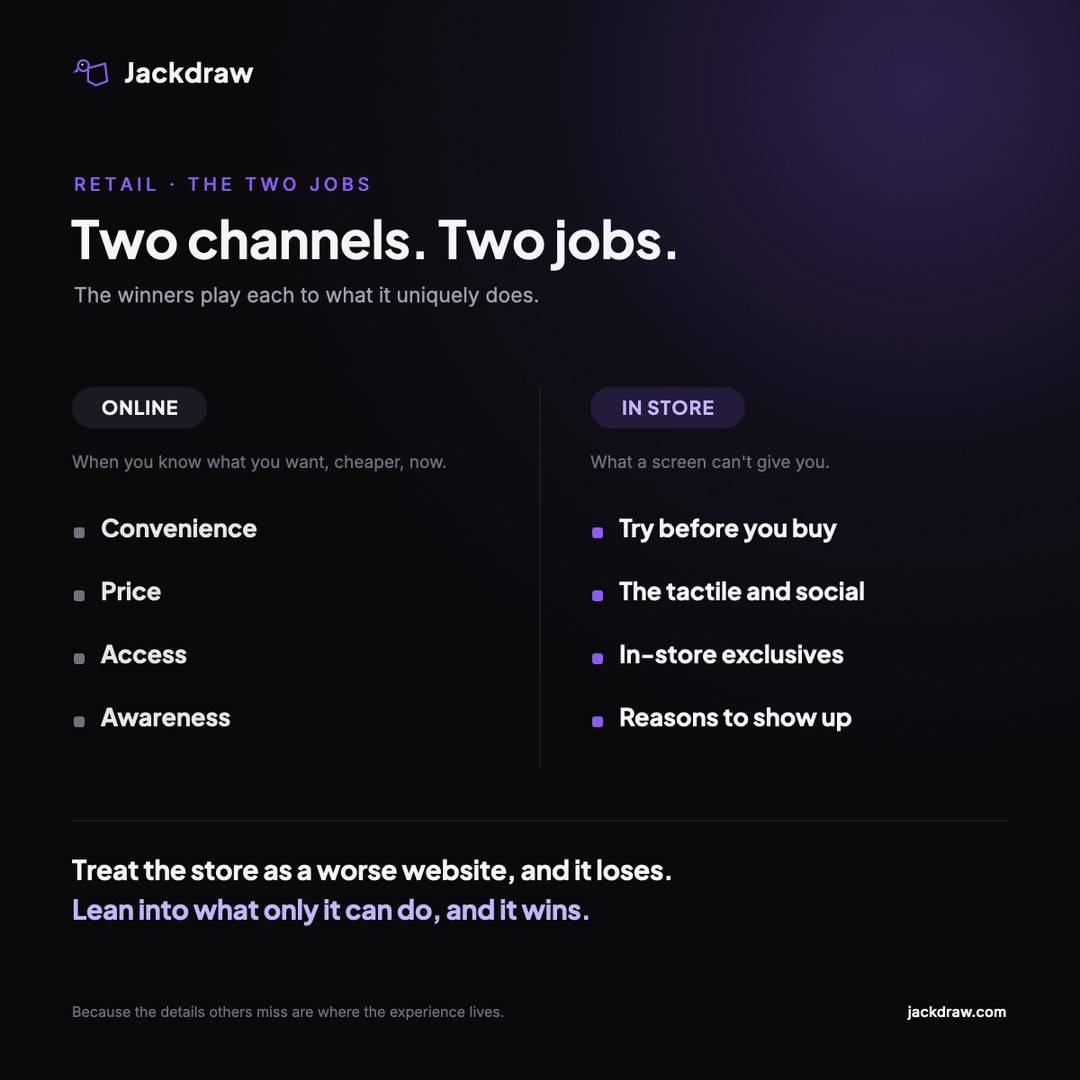

Online wins on convenience, price, access and awareness. It is where you go when you know what you want, or you want it cheaper, or you want it now. The store wins on everything online can't do: trying before you buy, the tactile and the social, and the reasons to show up that exist nowhere else.

When a retailer treats its store as a worse version of its website, a warehouse with a fitting room, it loses, because the website already does convenient better. When it leans into what only the store can do, it wins. The store isn't the problem. An under-used store is.

Digital's real job

The retailers pulling ahead aren't using digital to replace the store. They're using it to make the store worth visiting, and to make the visit effortless once you're there.

Uniqlo is the clearest example I've seen. Its stores are becoming service hubs, not just shelves: click and collect with in-store locker pickup, two-hour express delivery in markets including Australia, and a single account that follows you across app, web and store.

It automates the edges. Its "Uniqlo To Go" vending machines, in airports and transit hubs, dispense travel essentials, Ultra-Light Down and HeatTech, through a touchscreen and a robotic arm, with a QR code to the full catalogue. A tiny, staffless store placed exactly where demand is, at a fraction of the cost of a shopfront. And it uses AI with a point: mood-based recommendation kiosks, and demand forecasting that trims overproduction.

None of it is technology for its own sake. Every piece either drives a person toward a touchpoint or removes friction once they're there. Digital serves the physical, and the physical gives the digital somewhere to land.

The store as destination

Ask any Australian who's shopped in Tokyo or Bangkok and they'll rave about the department stores. Not because the products are cheaper, but because the stores are an experience. They've woven in food halls, viral hospitality and entertainment until the store stops being somewhere you buy and becomes somewhere you go. The shopping is almost a by-product of the visit.

Australia has its own version, and Mecca is one of the sharpest examples. Its Beauty Loop rewards are collected in store, a small, deliberate reason to walk in rather than click. Its new Bourke Street flagship in Melbourne, 4,000 square metres across three floors, is built as an all-day destination: a sprawling fragrance hall, a piercing studio, a skin clinic and treatment spaces, alongside more than 200 brands. You don't go there for a lipstick you could order in ten seconds online. You go for what the app can't give you.

It also shows how far there still is to go. Some of those service spaces read more as a new way to try product than a fully realised experience in their own right. That's less a criticism than a marker of where the bar is heading. As online keeps absorbing the transactional end of retail, the physical has to become genuinely worth the trip, not just a nicer showroom.

The biggest opportunity Australian retail leaves on the table is partnership. Overseas, retailers build symbiotic relationships with the businesses their customers already love: a cafe or restaurant inside the store, a service that fits the brand's world, so a visit becomes an hour rather than five minutes. Locally it's rare. Culture Kings is the exception that proves the point, building barbershops, DJs, a basketball half-court and a whole streetwear world into its stores, so a customer comes in for a haircut and a look, not a single hoodie. The service and the product sell the same lifestyle, and the store becomes the place that lifestyle lives.

The idea most retailers have backwards

There's a deeper move here that most retailers run in reverse.

The default is to put the exclusives and the convenience online, and let the store become a pickup point. The smarter play is the opposite: use the physical world for scarcity and experience, and let digital amplify it.

Sneaker culture is the purest version. A limited release, a queue down the street, an app drop that sells out in seconds. The scarcity is physical and time-bound, and it manufactures demand that spills across every channel: the resale market, the social feeds, the sheer want. The drop becomes the event. Digital just carries the noise.

There's an Australian angle worth testing. Uniqlo's vending concept makes obvious sense in dense Asian transit hubs. But a staffless, automated micro-store is just as interesting inside a major Australian shopping centre or flagship, where it's protected, sits in front of existing foot traffic, and extends the brand into spaces a full store could never justify. Automation doesn't have to mean removing the store. It can mean extending it.

Where this meets the experience

Here's where it connects to what we measure.

Omnichannel is usually treated as a feature checklist: click and collect, buy-online-return-in-store, an app, a loyalty card. Almost everyone can tick those now. Having the features is table stakes.

What separates the winners is whether the channels are actually one journey. Does the app know what's in your local store. Does click and collect take thirty seconds or thirty minutes. Does the store recognise the customer the app already knows. That is quality, not coverage, and it is exactly the gap our benchmarks keep finding: the fulfilment moat, the app divide, the seams between systems that customers feel and brands don't see.

The bottom line

Physical retail isn't dying. Discretionary retail is under genuine pressure, and the shift online is real. But the answer to a squeezed store isn't to abandon it. It's to give people a reason to walk in, and to make digital the thing that gets them there and smooths the way.

Digital's job was never to replace the store. It's to make the store worth the trip. Because the details others miss, the seams between the app and the aisle, are where the experience actually lives.

See where your experience really stands

Jackdraw publishes independent UX benchmarks of Australian industries, scoring the leading brands on what they've built and how well it's executed.

Browse the benchmarks →Sources: Deloitte Access Economics retail forecasts; ABS retail trade and household spending; CBRE and IBISWorld on online penetration; Ragtrader on department stores; Ogmento on Uniqlo's strategy; Mecca and Culture Kings store details from the brands' own pages and press coverage (Broadsheet, Time Out, ArchitectureAu).

Michelle Sawyer is the founder of Jackdraw, which publishes independent UX benchmarks of Australian industries.