Open any two major Australian retail websites side by side and something becomes obvious fast: they can do almost the same things. Search and filters, rich product pages, saved carts, click and collect, buy-now-pay-later, live chat, an app with push notifications and a loyalty program. The feature list has quietly become a checklist, and nearly everyone has ticked the boxes.

When we benchmarked 36 leading Australian retailers on two axes, functionality and experience quality, that convergence showed up plainly in the numbers.

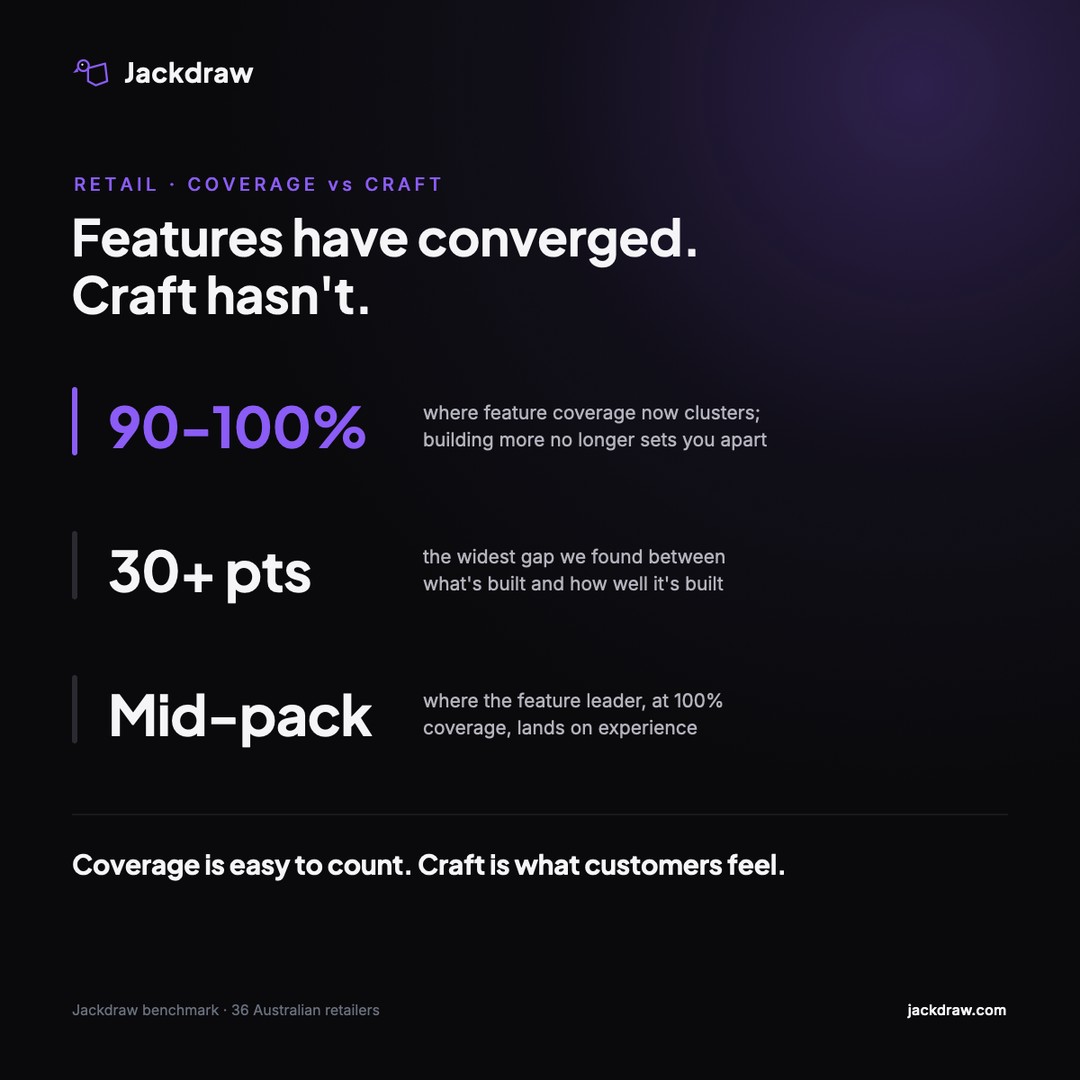

On functionality, the field bunches tightly at the top. Coverage clusters between 90 and 100 percent. Kmart has built the most of anyone, 100 percent of the criteria we scored, and most of its competitors aren't far behind. Having the features is no longer the achievement it once was. It is table stakes.

On experience quality, how well all that functionality is actually executed, the field spreads from the mid-50s to the low-80s. Same features, very different experiences. Kmart, the coverage leader, sits mid-pack on quality. The brand that leads overall, Decathlon, gets there not by having the most, but by pairing near-top coverage with the best experience quality of any retailer.

That gap, between what a retailer has built and how well it is built, is the whole story of where retail competes next.

Why everything started to look the same

Homogenisation didn't happen by accident. A few forces drove it.

Platforms did most of the work. When everyone builds on the same commerce platforms and plugs in the same best-in-class tools for search, payments, reviews and returns, everyone ends up with the same capabilities. That is a good thing for shoppers. It is a hard thing for brands trying to stand out.

Then there is the checklist mentality. Roadmaps get built by looking at what the category leader shipped last quarter and matching it. Feature parity feels safe. Nobody gets fired for adding the thing the competitor already has.

And it is about to accelerate. Meta just open-sourced Astryx, a free, production-ready, accessible-by-default component library. When anyone can assemble a polished, modern interface in an afternoon, the components themselves stop being a point of difference. The raw materials of a good-looking site are becoming free and universal.

So if the features are converging and the building blocks are commoditising, the obvious question follows: what is actually left to compete on?

Quality, not coverage

The answer is quality. The part shoppers actually feel.

Coverage is easy to count. You can put it on a roadmap and tick it off. Quality is harder, because it lives in the details: the checkout that doesn't stumble, the policy you can find without hunting, the page that loads and just works, the promo density that informs instead of shouting. In our benchmark, the widest coverage-to-quality gaps reached more than thirty points. That gap is money spent on features shoppers never feel.

Closing it beats adding to it. Here is where I'd point the effort.

- 01

Fix quality before you add features

Audit whether what you have already shipped is executed well. Promo clutter, buried policies, opaque checkout and slow pages are the most common quality deductions, and none of them are solved by building something new.

- 02

Treat accessibility as the differentiator it now is

Accessibility was the single weakest area in every retail category we scored, averaging 55 percent. It is also now a legal requirement under the EU Accessibility Act for any retailer selling to EU customers. Most brands are failing it, which means getting it right is both a compliance win and a genuine edge.

- 03

Own the fulfilment and returns experience

Features converge, but how a retailer handles delivery, pickup, and the two-way journey of a return is still where real separation happens. It is operationally hard, which is exactly why it is defensible.

- 04

Move to the visualisation frontier

Product video, user-generated content and richer visual merchandising still have low adoption. The next advantage on the product page is showing the product better, not adding another badge to it.

- 05

Make the app a first-class product

Increasingly the loyalty and the repeat purchase live in the app, and app quality splits the field sharply, so the brands that treat it as a first-class product, not an afterthought, are the ones that pull ahead.

- 06

Compete inside your category, not against the whole field

The overall leaderboard flatters breadth. Your shoppers compare you to your direct peers, in your category, not to the retailer with the most features across the market. Read your category league, and win it.

The bottom line

For a decade, the retail digital race was about building more. That race is largely over, and most of the field finished it. The features are converging, the building blocks are becoming free, and having a capability no longer sets you apart.

What sets you apart now is how well the whole thing is executed, whether every shopper can use it, and whether the moments that matter, the checkout, the return, the reorder, feel considered rather than assembled.

Features are table stakes. The experience is the moat. Because the details others miss are where the experience actually lives.

See where your experience really stands

The Australian General Retail, Fashion and Fast Food benchmarks score the leading brands on what they've built and how well it's executed.

Browse the benchmarks →Source: Jackdraw's benchmark of 36 leading Australian retailers, scored on functionality and experience quality across web and app against 13 established UX frameworks.

Michelle Sawyer is the founder of Jackdraw, which publishes independent UX benchmarks of Australian industries.